Press Release

June 1, 2026

SBI Sumishin Net Bank, Ltd.

SBI Sumishin Net Bank Launches Japan’s First “Hybrid Mortgage Loan” Offered by a Mega Bank or Internet Bank

A New Mortgage Structure for Condominiums Combining Regular Repayments with a Lump-Sum Payment at Maturity

SBI Sumishin Net Bank, Ltd. (Head Office: Minato-ku, Tokyo; President & CEO: Noriaki Maruyama; henceforth referred to as “SSNB”) today announced the launch of a new condominium-focused mortgage product, the Hybrid Mortgage Loan with Partial Lump-Sum Repayment at Maturity, the first of its kind to be offered by a mega bank or an internet bank in Japan (*).

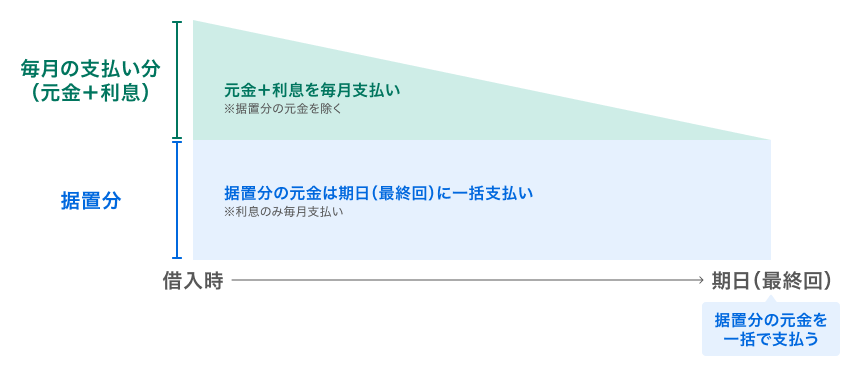

Against the backdrop of rising condominium prices, particularly in central urban areas, and changing lifestyles, SSNB has developed this new mortgage structure to address increasingly diverse financing needs when purchasing a home. The product combines regular monthly repayments with a lump-sum repayment at a predetermined maturity date, while allowing a portion of the principal—equivalent to 50% of the collateral valuation—to be deferred.

This mortgage is SSNB’s proprietary hybrid product, combining conventional repayment methods—either equal total payment (principal and interest) or equal principal repayment—with a lump-sum repayment at maturity.

By reducing the monthly repayment burden, the new mortgage offers customers greater flexibility in acquiring high-value condominiums and in responding to future changes such as relocation or evolving life stages.

New Hybrid Mortgage Loan

Background to the Development

As condominium prices continue to rise in central urban areas, demand—particularly among the working generation—for properties with strong asset value has been increasing. At the same time, higher monthly mortgage repayments are placing growing pressure on household finances.

To address this challenge, SSNB has previously offered products such as 50-year mortgages designed to reduce monthly repayment burdens. However, due to age limits at loan maturity, the availability of such ultra-long-term loans has been restricted to a limited segment of customers.

In addition, an increasing number of customers are choosing to relocate as their life stages change, often involving the sale of their existing properties. As a result, interest in acquiring homes with high asset value has continued to grow. There is also demand for properties with a predetermined ownership period, such as those with fixed-term land lease rights.

Against this backdrop, SSNB has developed a hybrid mortgage product that reduces monthly repayment burdens while supporting the acquisition of high-value properties. The Bank has commenced offering this product for both newly built and pre-owned condominiums.

While the product is initially available for condominiums, SSNB plans to further enhance its features in response to customer needs, including expanding eligibility to detached houses.

By offering greater flexibility to accommodate life events such as career transitions, family growth, and future relocation, and by expanding customers’ options not only for today but also for the future, SSNB remains committed to supporting long-term asset formation.

Commencement Date

June 1, 2026 (Monday)

Product Overview

This mortgage product combines a repayment structure under which a portion of the principal equivalent to 50% of the collateral valuation is repaid in a lump sum at a predetermined maturity date (the lump-sum-at-maturity portion) with a conventional mortgage repayment structure for the remaining principal.

For the portion subject to lump-sum repayment at maturity, borrowers are required to pay interest only during the loan term. The remaining principal is repaid through standard mortgage methods—either equal total payment (principal and interest) or equal principal repayment.

By combining these two repayment methods, the product enables borrowers to reduce their monthly repayment burden

Repayment Illustration

| Product Name | Hybrid Mortgage Loan with Partial Lump-Sum Repayment at Maturity |

|---|---|

| Eligible Borrowers | Applicants who meet all of the following criteria: • Aged 18 to 65 at the time of borrowing and under 80 at loan maturity • Previous year’s annual income of JPY 10 million or more (for pair loans, either borrower must meet this requirement) • Eligible to enroll in the Bank-designated group credit life insurance • Residents of Japan |

| Purpose of Funds | Purchase of a residential condominium for occupancy by the borrower or family members, including related expenses |

| Eligible Properties | Service Areas: Tokyo 23 Wards; Yokohama City; Kawasaki City; Osaka City Property Type: New or pre-owned condominiums with a collateral valuation of JPY 100 million or more Property Age: Up to 65 years old at loan maturity |

| Loan Amount | JPY 5 million to JPY 300 million (in increments of JPY 100,000) |

| Loan Term | Up to 35 years |

| Interest Rate Type | Variable interest rate or fixed-rate option |

| Interest Rate | Additional margin of 0.350% (as of June 2026) The interest rate applicable on the loan execution date will apply. |

| Repayment Method | Equal total payment or equal principal repayment plus lump-sum repayment at maturity |

| Group Credit Life Insurance | Enrollment in the Bank-designated group credit life insurance plan “Sugo Danchin” (underwritten by SBI Life Insurance Co., Ltd.) is required |

| Administrative Fee | 2.20% of the loan amount (tax included) |

| Collateral | A first-ranking mortgage in favor of the Bank will be established on the financed property |

Who This Product Is Designed For

This mortgage product is designed for customers considering the acquisition of high-asset-value condominiums in central urban areas and major metropolitan regions, who seek to reduce their monthly repayment burden while maintaining flexibility to prepare for future relocation or changes in life stages.

For example, the product is well suited for customers who:

- Face difficulty in utilizing ultra-long-term mortgages due to age limits at loan maturity

- Anticipate relocating within the next 10 to 15 years

- Wish to expand future options in light of changes in childcare needs or working styles

- Seek to maintain a highly convenient living environment over the long term

Important Notes Regarding Use

- Applications for this product must be submitted through authorized agents or partner companies. For further details, please contact SSNB or its authorized agents. Detailed product information is also available in the product overview document published on the Bank’s website.

- All applications are subject to the Bank’s prescribed screening process. Depending on the results of the screening, the Bank may not be able to accommodate all applications.

- Interest rates are reviewed monthly. The applicable interest rate will be the rate in effect on the loan execution date, not the application date, and may therefore differ from the rate at the time of application.

- This product is not available for online application.

- Loan agreements will be executed in written form. Written contracts are subject to stamp duty under Japanese tax law.

- This product does not guarantee future property values. Borrowers are required to repay the full loan amount by the maturity date.

- ※ (*) Based on research conducted by SSNB as of May 27, 2026, using information disclosed on the websites and publicly available materials of the following financial institutions: Mizuho Bank; MUFG Bank; Sumitomo Mitsui Bank; Resona Bank; PayPay Bank; Seven Bank; Sony Bank; Rakuten Bank; au Jibun Bank; AEON Bank; Daiwa Next Bank; Lawson Bank; GMO Aozora Net Bank; MinnaBank; and UI Bank. Early repayments are excluded.

Contact

For further information about this press release, please contact:

SBI Sumishin Net Bank, Public Relations

kouhou_pr@netbk.co.jp

Note: This content has been translated from the Japanese original using AI-assisted machine translation for reference purposes only.

In the event of any discrepancy between this translated document and the Japanese original, the original shall prevail.